What should your business be doing if you’re worried about insolvency?

By Mr Bankruptcy

29th April 2020

In March, The Independent newspaper reported that almost a fifth of UK’s small businesses could be gone within a month due to the financial crisis caused by Covid-19 restrictions. This is despite the billions of pounds of support being made available by the UK Government and the changes made to insolvency legislation to help company directors stay afloat during lockdown.

Now we know the extent of the crisis, I believe the Independent’s prediction is overly pessimistic; companies are adapting, improvising and overcoming to a greater extent. However, these are undoubtedly tough times for any business, large or small, and a business owner should be prepared to take action or seek help if necessary to survive.

Temporary changes to Insolvency legislation

To help directors avoid insolvency, temporary changes have been announced and it would be a good idea to be familiar with them:

- A temporary suspension of wrongful trading rules to allow directors to continue trading during the pandemic and save their business without the threat of personal liability should the business eventually become insolvent.

- Breathing space from creditors enforcing debt repayment whilst companies work to restructure or look for rescue.

- A new restructuring plan that commits creditors to the plan.

- Protection against being cut off from supplies and services which are essential for the business to keep trading.

The next steps if your business is struggling

The current circumstances are unique but the main causes of insolvency remain constant. We’ve previously discussed why businesses become insolvent, including the signs to watch out for, and many of these still hold good. If you’re concerned that you’re in this situation, here are some essential keys steps to take:

- Ensure you have all the facts and figures clear and correct so that you understand the scale of the issues you need to resolve.

- If you’re a company director, understand your legal duties and obligations if your business becomes insolvent.

- Talk to an expert and seek advice as soon as possible. Although talking about debt is not always comfortable, without expert advice you may not fully understand your situation, the potential options available to you and the impact of each of them.

- Don’t do nothing. When you’ve understood your options, choose one and take action; the problem won’t go away until you do this.

If we’re going to turn the economy around as quick as possible once the pandemic restrictions start to ease, it’s vital that as many businesses as possible survive the coming weeks, or possibly months, of restricted trading, and that could be down to owners and directors taking early action.

James Rosa Associates

James Rosa associates is a firm of debt advisors and debt adjustors. With a supportive and friendly approach, we offer a full range of advice and professional services to individuals and business owners/directors facing unmanageable debt or involved in civil or commercial disputes.

Our services include:

● Insolvency support

● Negotiated settlements

● Personal assisted bankruptcy

● Mediation

We are authorised and regulated by the Financial Conduct Authority (FRN665061) to work with clients to produce bespoke solutions to fit their specific circumstances.

Find out if you qualify for a free consultation

If you want to deal with an unmanageable debt, or bring a dispute to a swift and cost-effective resolution, contact James Rosa Associates, ring 0845 6807217 or email enquiries@jamesrosa.co.uk to find out whether you qualify for a free consultation.

What should businesses be doing during the coronavirus pandemic to protect themselves?

By Mr Bankruptcy

20th April 2020

Many businesses are learning to switch from business as normal to a day-to-day routine that’s managing change, repurposing resources and mitigating risks raised by Coronavirus. In my role as a debt advisor and adjustor I see a lot of what companies do, and fail to do, when it comes to keeping their finances healthy. So, to help adjust to current times here are some business tasks to be thinking about.

Areas of focus to help businesses

- Review your business plans: Revisit your business and financial plans and make adjustments to help ensure your business’s short term, and longer term, viability. It’s essential to reassess your situation in the current context to address the risks.

- Know what support is available: The Government has introduced an eye-watering range of measures from support with employee payrolls to deferring VAT payments. Some support are grants, some loans and some deferred payments, but research them all – they could be vital to ensure your business survives.

- Use online resources: Many organisationshave rallied to pull resources together to offer guidance to businesses. Find trusted and reliable sources such as trade associations, specialist advisers and business federations to get inspiration and learn new ideas that could help your business.

- Review your insurance policy: Understand the level of protection offered by your insurance policies as these may offer some much-needed relief support.

- Support from Banks: Talk to your bank to understand what they can offer you, including business interruption loans, help with credit cards payments, etc.

- Keep planning for the long term: Short term needs may require your immediate attention but don’t forsake planning for the future. Be clear on how you’ll drive your business forward as the situation changes and we begin to rebuild the economy.

- Ask for help, quickly: If you have concerns when revisiting your business and financial plans, seek help as soon as possible. This could mean you have more options available to you than you think to address issues. It can also help you avoid the physical and mental impact of the pressure that any business owner is going to find themselves under and identify a possible path forward.

Whatever your situation, there is support and advice available. At James Rosa Associates we see a lot of businesses tackling difficult times and we know the positive impact that simply talking about your challenges has, to let you regain control.

James Rosa Associates

James Rosa associates is a firm of debt advisors and debt adjustors. With a supportive and friendly approach, we offer a full range of advice and professional services to individuals and business owners/directors facing unmanageable debt or involved in civil or commercial disputes.

Our services include:

● Insolvency support

● Negotiated settlements

● Personal assisted bankruptcy

● Mediation

We are authorised and regulated by the Financial Conduct Authority (FRN665061) to work with clients to produce bespoke solutions to fit their specific circumstances.

Find out if you qualify for a free consultation

If you want to deal with an unmanageable debt, or bring a dispute to a swift and cost-effective resolution, contact James Rosa Associates, ring 0845 6807217 or email enquiries@jamesrosa.co.uk to find out whether you qualify for a free consultation.

What does the future hold?

9th April 2020

As I am writing this, we find ourselves in the middle of a lockdown due to the COVID-19 pandemic. Needless to say, these are unprecedented times and nobody can be certain what the future holds.

A lot of people have said to me that I must be really busy at the moment given I specialise in personal debt advice and helping people through bankruptcy. Strangely enough, actually quite the opposite is currently true (at least in the immediate term). There are a number of interesting things to consider here:

- Creditors have had their hands tied behind their back somewhat with courts adjourning petitions (e.g. winding-up, bankruptcy, evictions etc) for 12 weeks. This would mean a significant build up of cases meaning it would likely be months before a creditor could get a debtor into court. There was a Practice Direction issued this week to mitigate this by having hearings done by telephone etc, but only time will tell if that alleviates pressure from the backlog.

- The Financial Conduct Authority (FCA) issued draft guidance on the 2nd April proposing to make amendments to CONC 6.7 by encouraging the provision of COVID-19 specific forbearance measures. Anecdotal evidence would also suggest that most lenders are keen to be seen to “do the right thing” no doubt in case they need a bailout at some point in the future themselves.

- With 3-month mortgage repayment holidays now being taken up, those who have cash are reluctant to let it go. Whilst this may help in the short term, the medium to long term impact right across the supply chain cannot be underestimated as individuals and businesses embrace the idea of not paying anyone.

- Everyone thinks the government will ride to the rescue. Given the fact that businesses are likely to have to wait until June for payment for the workers that have now been furloughed, how many businesses have those kind of cash reserves? Others are of the opinion that they only need to make a call and they’ll get a £10k cash grant. Even more worrying is the new Coronavirus Business interruption Loan Scheme (CIBILS) which sounds fantastic, but many lenders are already indicating it will be 3 months before they have a chance to look at new applications.

So, what happens next?

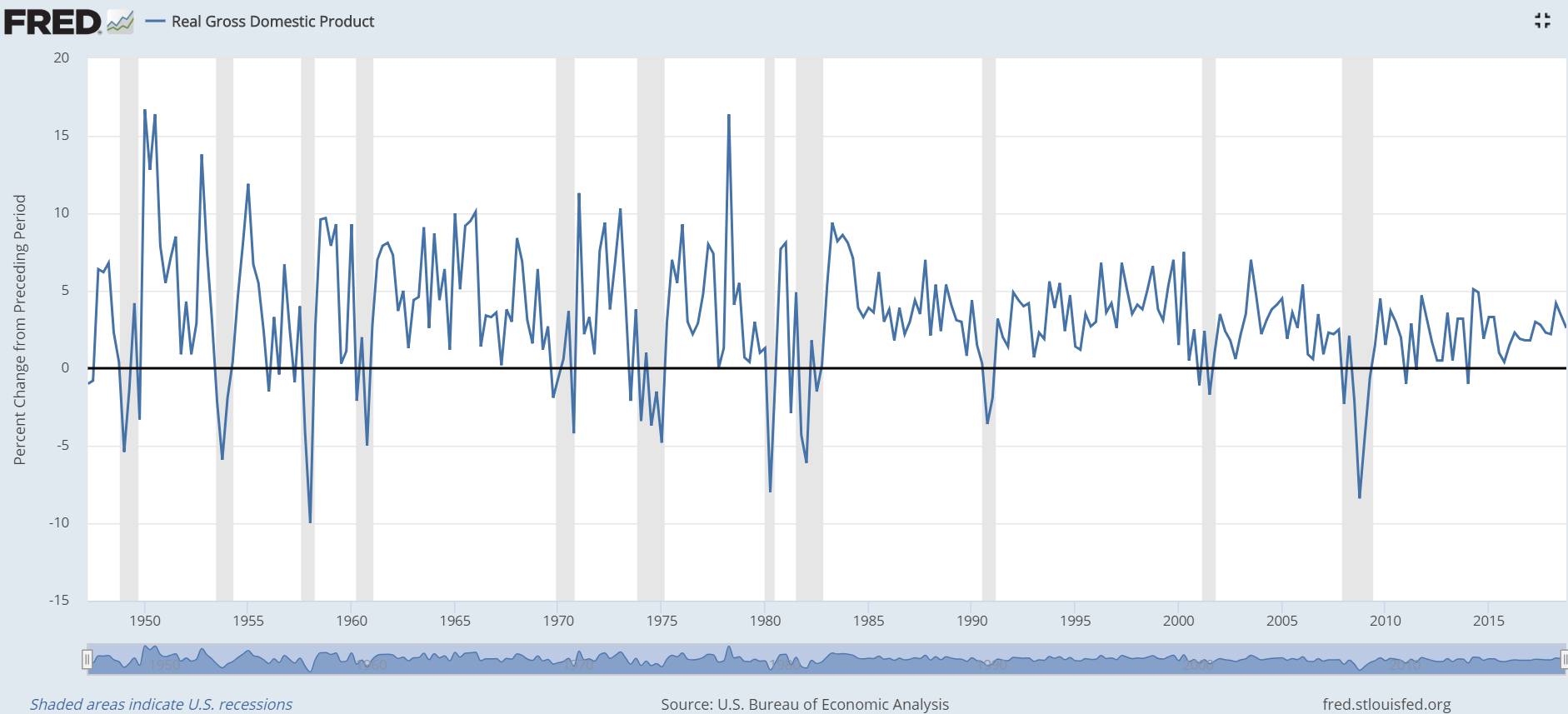

I think it is likely that in 45-60 days, large numbers of businesses and individuals are going to be running out of cash (if they haven’t already done so) and in 60-90 days, we will see a spike in formal insolvencies (both personal and corporate). By the time this lockdown is over, I believe that rather finding ourselves in recession, we will be in a global depression whose effects may last the best part of 10 years. Given that most governments and central banks have used their arsenal of tools to combat the last economic crash (QE, interest rate cuts etc), there will not really be anything left in the locker to deal with the economic aftermath of this pandemic.

What can we do now?

Now is the time to really take a look at your financial situation whilst you are not under creditor pressure. The problems are not going to go away because of the pandemic, but the can has just been kicked a few weeks down the road. Do your research and have a plan.

As an example, I was speaking to a potential client who sadly has found personal bankruptcy is inevitable. They were considering when the best time to start the process was and I advised them that now is the time. As you are kept in bankruptcy for 12 months, why not “serve” some of that time during the lockdown when you can’t do anything else anyway? By the time things start getting back to normal, you will be almost through the process.

Finally and in the immortal words of Douglas Adams, DON’T PANIC !